Custom CRM for Insurance Brokers and Agencies

7 min read · AstraLoop Studio

If you run an agency or work as an insurance broker, your problem isn't finding a tool to save contacts. The problem is that the value of your work rests entirely on continuity. A policy that expires and isn't renewed is a client walking out the door, often without anyone noticing until it's too late. And standard business software, built for accounting or for a single line of business, doesn't help you manage that cycle.

A custom CRM for insurance brokers and agencies isn't a luxury reserved for big groups. It's the infrastructure that ties together the two halves of your business: on one side the renewal engine (portfolio, deadlines, cross-selling), on the other the acquisition of new clients. In this article we look at what it actually needs to do, where generic software falls short, and when it's worth building one tailored to you instead of adapting someone else's.

Why Excel and standard software aren't enough

Almost every agency starts with the same setup: the insurer's own software (or two, or five, one per mandate), an Excel file for deadlines, and the owner's memory for everything else. It works while the portfolio is small. Then it grows, and the cracks start to show.

The limits are structural, not a matter of discipline:

- Data scattered across multiple mandates. Client Smith has car insurance with one company, home insurance with another, professional liability with a third. No single system shows you the full picture of that client, so you miss both cross-selling opportunities and warning signs of churn.

- You chase deadlines by hand. Excel doesn't warn you. You're the one who opens the file every Monday morning, filters by month, and hopes you haven't skipped a row. One week of holidays or a busy spell and a renewal slips through.

- No record of conversations. Did you call the client back who wanted to think it over? Did you send the updated quote? If the answer only lives in the head of the colleague who's off today, that information effectively doesn't exist.

- Acquisition is disconnected from management. Leads coming from the website or campaigns end up in an inbox or another spreadsheet. The move from "interested contact" to "client with an active policy" isn't tracked, so you don't know what acquisition actually costs you or where you're losing people along the way.

The result is that you spend more time gluing systems together than selling and advising. And it's exactly the kind of repetitive work that can be removed with well-designed business process automation.

What a CRM for insurance brokers needs to do

A CRM that actually works for insurance stands on two legs. The first is managing the existing portfolio, where the safest margin lies. The second is acquisition, which fuels growth. Let's look at them separately, since they call for different logic.

1. Client records with linked policies

The heart of the system is the client record that pulls everything together: personal details, family or company, and every active policy with its line of business, insurer, premium, start date, expiry and payment schedule. Open the Smith file and you see three policies, that car insurance expires in 40 days, and that they have no accident coverage. At a glance you get both the renewal reminder and the sales opportunity.

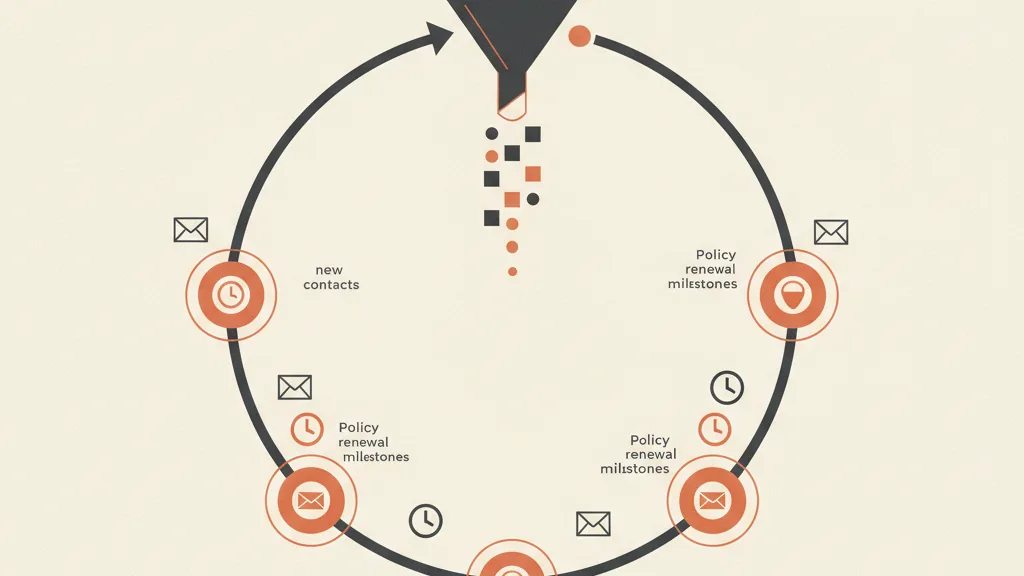

2. A deadline and renewal engine

This is the feature that pays for the CRM on its own. The system needs to calculate deadlines automatically and trigger a sequence of actions before the term arrives. A typical workflow looks like this:

| Timing | Automated action |

|---|---|

| 60 days before | The broker receives the month's renewal list, prioritized by high premiums and at-risk clients |

| 45 days before | Email or WhatsApp message to the client with a notice and an offer to review their coverage |

| 20 days before | If there's no response, the system creates a call-back task assigned to the operator |

| After expiry | If the renewal hasn't happened, the client enters a priority recovery list |

This isn't rocket science. It's the same logic as automated sales follow-up, applied to the policy lifecycle. The gap between an agency that renews 90% of its portfolio and one that loses 15% every year is often exactly this.

3. Managing quotes and open negotiations

Every quote that goes out should have a status: sent, pending, accepted, lost. Without this, unclosed quotes simply vanish. A well-built CRM tracks every negotiation and automatically re-engages the ones that have gone stale, the same way automatic recovery of unclosed quotes works. For a broker this matters twice as much, because a client who asks for a quote and then disappears often just needs a nudge at the right moment.

4. Integration with acquisition channels

This is where the loop closes. Leads coming from campaigns, the website or word of mouth need to land directly in the CRM, not in a separate tool. Every new contact gets qualified, assigned and followed up with a dedicated sequence. If you're working on this front, it's worth first understanding how lead generation in the insurance sector is structured, where response time and qualification matter more than raw contact volume.

The advantage of having acquisition and management in the same system is that the funnel feeds directly into the CRM: the lead becomes a client, the client enters the renewal cycle, and at expiry re-enters the cross-selling engine. One single, measurable flow from start to finish.

5. Compliance and traceability (IVASS and GDPR)

The sector is regulated: suitability of the proposal, questionnaires, the pre-contractual information document, traceability of consents. A custom CRM can build your obligations into the flow itself, archiving the right documents at the right time and keeping a history of data-processing consents. This isn't legal advice (for IVASS and GDPR obligations always refer to current regulations and your own advisor), but designing the system around compliance from the start means you're not chasing it afterward.

Custom CRM or off-the-shelf insurance software?

The right question isn't "custom versus standard" in the abstract, but what your agency actually needs. Here's an honest comparison:

| Aspect | Off-the-shelf vertical software | Custom CRM |

|---|---|---|

| Time to launch | Fast | Longer (there's a design phase) |

| Fit with your mandates and processes | You adapt to the software | The software adapts to you |

| Acquisition + management integration | Often missing or clunky | Native, it's the core idea |

| Cost over time | Per-user license, grows with the team | Upfront investment, then lower running costs |

| Custom automations | Limited to what's built in | Modeled on your actual workflow |

The rule of thumb: if you work with a few standardized lines and just need to manage deadlines, an off-the-shelf vertical tool can be enough. But if your value lies in processes that are yours (portfolio segmentation, structured cross-selling, an integrated acquisition funnel), standard software becomes a cage. We covered this fork in the road in more depth in custom vs. standard CRM: which to choose, worth reading if you're still on the fence.

Want to see how a CRM built around your portfolio would cut down on missed renewals? Request a free analysis of your deadlines-renewals-acquisition cycle.

How much it costs and how long it takes

These are the two questions I always get asked. On price: a custom CRM for an insurance agency isn't bought off a shelf, so the cost depends on the number of integrations (how many insurer systems you need to connect), the complexity of the automations, and the acquisition component. For a concrete sense of the order of magnitude, we wrote a dedicated guide to the cost of building a custom CRM, with real ranges and no hand-waving.

On timing: a system covering portfolio, deadlines and renewals can be up and running in a few weeks for a working first version, then extended in phases (acquisition, advanced cross-selling, reporting). You don't need to wait for it to be "complete" to start using it: you'll see the value on renewals from the very first automated deadline campaign. If you want to understand timelines in general, here's how long it takes to implement a CRM.

Where to start

The practical advice is not to start from the software, but from your own cycle. Grab a pen and paper and map out what happens from the moment a contact comes in to the moment a policy expires and needs renewing. Where does information get lost? Which steps do you do by hand every week? Which clients left last year, and why?

That map is the spec for your CRM. A good custom CRM with an integrated funnel is nothing more than that map translated into a system that works for you, instead of the other way around. Less time gluing Excel and other software together, more time advising clients and bringing in new ones.

The portfolio you already have is your most valuable asset. Protecting it from missed renewals and growing it through cross-selling is worth, almost always, more than any new campaign. A CRM built around your work is what makes all of this possible systematically, instead of relying on memory.

Frequently asked questions

Does a small insurance agency also need a custom CRM?

Yes, often even more so. In small agencies, deadlines and follow-ups depend on the memory of one or two people, and that's exactly where renewals get lost. A custom CRM, even in a scaled-down version, secures the portfolio without depending on any single person.

Does the CRM integrate with insurers' own systems?

It depends on what each insurer makes available (APIs, exports, data feeds). A custom CRM is designed around the mandates you actually hold, connecting via integration where possible and via structured import where insurers don't offer direct access. It's one of the points to define during the analysis phase.

How does it handle policy deadlines and renewals?

The system calculates deadlines automatically and triggers a sequence of actions before the term arrives: alerts to the broker, communications to the client by email or WhatsApp, and call-back tasks if there's no response. That way no renewal depends on remembering to check a spreadsheet by hand.

Does an insurance CRM also handle new client acquisition?

A well-designed custom CRM does. Leads from the website, campaigns or referrals go straight into the system, get qualified and followed up with dedicated sequences, and once they become clients they enter the renewal cycle. Acquisition and management live in the same flow, not in separate tools.

How much does it cost to build a custom CRM for a broker?

There's no single price: it depends on the number of integrations with insurers' systems, the complexity of the automations, and the acquisition component. The most reliable way to get a figure is an analysis of your actual workflow. You can start with a working version and expand it in phases.

Is it compliant with IVASS and GDPR requirements?

A custom CRM can build your obligations into the workflow: archiving pre-contractual documents, tracking consent to data processing, keeping a history of communications. For specific requirements always refer to current regulations and your own advisor, but the system can be designed to help you meet them.

Tell us how your agency works today: we'll map out the flow together and tell you, with no obligation, what we'd automate first.